外国人が日本の不動産を持ったまま死亡した場合、相続人に相続税の申告義務が生じることをご存知ですか?If a foreign national passes away owning real estate in Japan, the heirs may be required to file Japanese inheritance tax — even if they live abroad.

外国人が日本の不動産を持ったまま死亡した場合、相続人に相続税の申告義務が生じることをご存知ですか?If a foreign national passes away owning real estate in Japan, the heirs may be required to file Japanese inheritance tax — even if they live abroad.

If you recently lost a spouse, parent, or family member who owned real estate in Japan, you may need to file and pay Japanese inheritance tax. This applies to foreign nationals and non-residents alike. Being a foreign spouse, child, or sibling of the deceased does not exempt you.

A common misconception is that “foreign nationals don’t have to pay Japanese inheritance tax.” In reality, Japan’s inheritance tax law classifies heirs as either “Unlimited taxpayers” or “Limited taxpayers.” Most foreign heirs fall into the “Limited taxpayer” category — and are still taxed on all assets located within Japan.

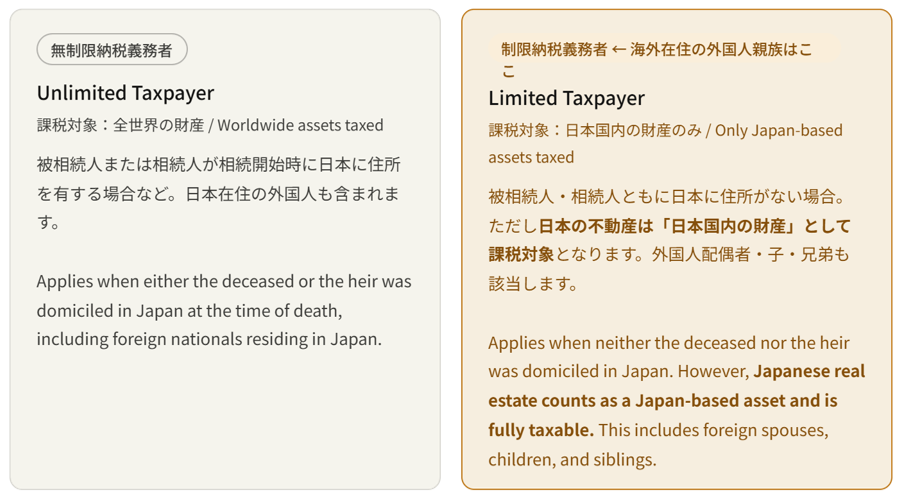

無制限納税義務者 Unlimited Taxpayer

課税対象:全世界の財産 / Worldwide assets taxed

被相続人または相続人が相続開始時に日本に住所を有する場合など。日本在住の外国人も含まれます。

Applies when either the deceased or the heir was domiciled in Japan at the time of death, including foreign nationals residing in Japan.

Applies when neither the deceased nor the heir was domiciled in Japan. However, Japanese real estate counts as a Japan-based asset and is fully taxable. This includes foreign spouses, children, and siblings.

海外在住の外国人であっても、日本の不動産を相続した場合 → 相続税の申告義務が生じます(制限納税義務者) Even living abroad, inheriting Japanese real estate triggers a Japanese inheritance tax filing obligation (as a “Limited Taxpayer”).

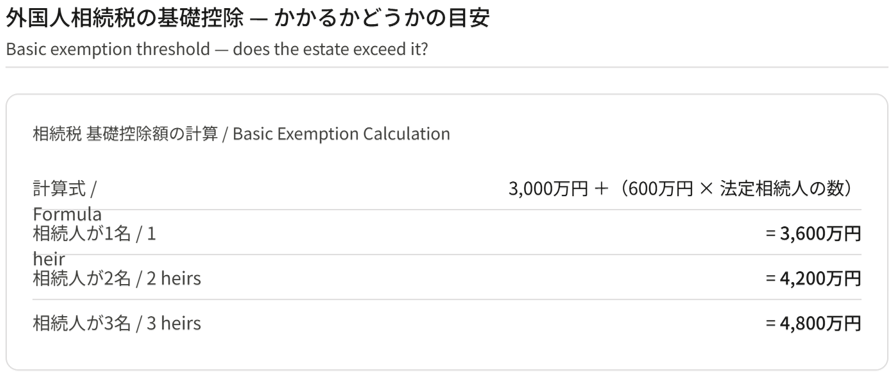

外国人相続税の基礎控除 — かかるかどうかの目安 Basic exemption threshold — does the estate exceed it?

Properties in Tokyo, Osaka, and other major cities frequently exceed these thresholds. Japan’s assessed value (路線価 / road price) is lower than market value, but many estates still require a filing. The belief that “foreign nationals don’t pay inheritance tax on Japanese land” is a myth — Limited taxpayers are fully liable for Japan-based real estate.

For inheritance procedures and asset division, the law of the deceased’s home country typically applies (choice of law). However, Japanese inheritance tax obligations are a separate matter — Japanese tax law applies to assets located in Japan, regardless of nationality.

If your spouse owned Japanese real estate and its assessed value exceeds the basic exemption, you and your children are required to file — even as foreign nationals. Japanese inheritance tax applies to Japan-based assets regardless of the nationalities involved.

Foreign nationals can also renounce their inheritance rights. The deadline is 3 months from learning of the death, and the application must be filed with a Japanese family court. Foreign documents (equivalent to a family register) and sworn affidavits may be required. Consult a professional promptly.

Since April 2024, inheritance registration (title transfer) has become mandatory in Japan. Foreign nationals are also subject to this requirement and must register within 3 years of learning of the inheritance. Foreign identity documents and affidavits are typically required in place of a Japanese family register. Note that the tax filing deadline (10 months) and registration deadline (3 years) are different.

For Limited taxpayers, only assets located in Japan are subject to Japanese inheritance tax. Overseas bank accounts and foreign real estate are generally excluded. However, Unlimited taxpayers are taxed on their worldwide assets.

申告に必要な書類(外国人の場合)Required documents for foreign national heirs

Foreign heirs must submit standard documents plus foreign-issued documents with certified Japanese translations. Requirements vary by country of origin.

日本側で必要な書類 / Japan-side documents

被相続人の戸籍謄本(除籍)

不動産の登記事項証明書

固定資産税評価証明書

遺言書(もしあれば)

遺産分割協議書

外国人相続人が追加で必要な書類 / Additional for foreign heirs

本国の出生証明書・婚姻証明書等

宣誓供述書(Affidavit)

パスポートのコピー

各書類の日本語訳(翻訳者の署名入り)

在外公館での認証が必要な場合あり

今すぐ確認すべきことWhat to do right now

亡くなった方が日本に不動産(土地・建物・マンション等)を保有していたか確認する

Confirm whether the deceased owned real estate in Japan (land, house, apartment, etc.)